How Credit Scoring Works

Credit scoring is used to help businesses decide if credit should be given, or to help with setting credit limits on credit or store cards and other lines of credit ie. loans.

Your credit score is based on how well you have previously paid off credit and this information is held on your personal credit file. Your credit score is mostly based on your credit report information and usually includes the following:

- Length of credit history: How long have you had credit accounts.

- Payment history: How often you made payments on time and how many (if any) late payments.

- Amount owed: How large or small were the lending amounts.

- Types of credit: Are the credit lines secured or unsecured, are any with utilities ie. power, phone, etc

- Asking for credit: How recent was your latest line of credit been opened and how many times have you asked for credit.

- Defaults, judgments, debt repayment orders & insolvencies: Do you have any on your credit report, how recent are they, amount outstanding etc.

The better the information on your credit score, the more positive your credit score will be:

If it looks like you have too much credit or are starting to show signs of not being able to pay or pay on time, this can have an impact and lower your credit score, even though you may not have missed any of your repayments.

Credit providers like banks, finance companies and utilities often use credit scores as part of their approval process. You may find that one provider will accept your applicantion at a particular score, while another may not. The policy of applying credit scores ensures a more consistent and fairer approach across all applicants and generally means more applications are approved as the credit provider has a greater level of awareness of the risk they are taking on.

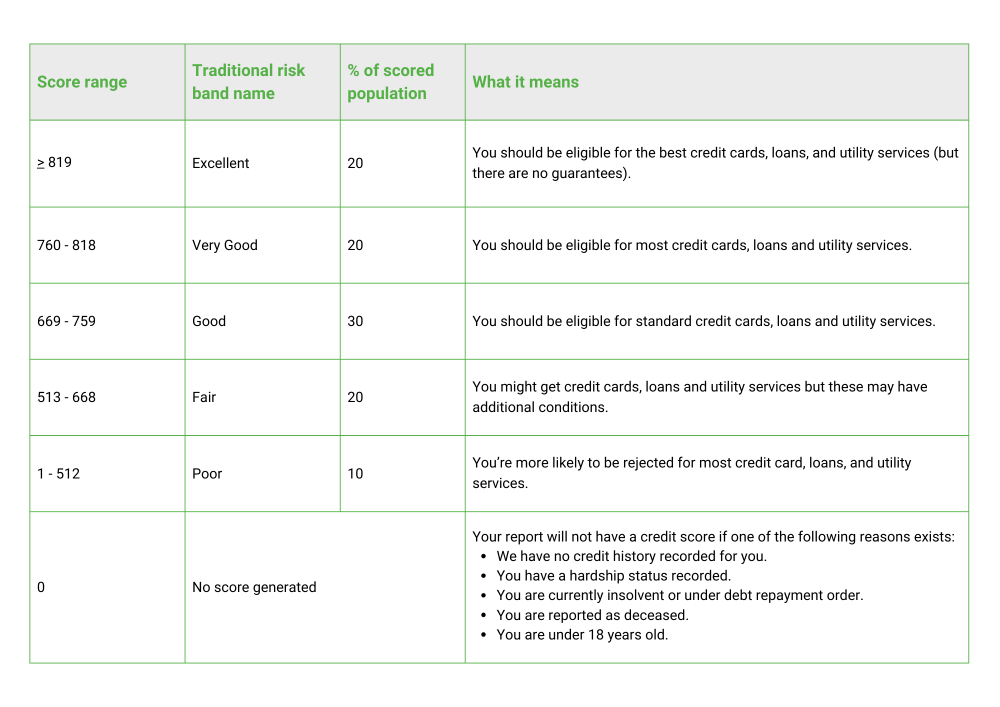

The Centrix consumer score ranges from 0 (for the very high risk) to 1,000 (for the very low risk) and the scores are spread across these five areas:

We provide free credit reports and Centrix consumer scores to help you understand what your personal credit rating looks like.

If you have any issues with any items on your credit score, you need to contact the provider of that issue i.e. the utility or loan provider to discuss this. Centrix cannot remove or change what is shown on your credit score, only the credit provider can do this for you.